[ad_1]

It’s not just people who make irresponsible investment decisions that believe shorting should be made illegal. Even His Holiness Elon Musk has been vocal about wanting to “go after the Wall St short-sellers,” his feud with Bill Gates allegedly surrounding a large Tesla short position. No matter how bad a company appears to be, we never short stocks because the irrationality of the meme stock types will always outlast our margin limits. In fact, we find short reports to be the ultimate bear case steel man that we can use to evaluate long positions.

We previously pointed out how AI hype was driving the price of C3 (AI) along with other AI-labeled stocks like Soundhound (SOUN) and the ultimate AI pick and shovel play, NVIDIA (NVDA). The excitement seems to have started in late January of this year, a point in time at which C3 traded around $12 a share. Nothing has happened over the past several months to merit the rocketing share price, so we have every reason to believe the intrinsic value of C3 remains roughly the same – the range of $12 a share that it was trading at before the hype hit.

Shares should return from whence they came, approximately $12 per share, or almost 60% below current levels. The company’s high mix of lower margin professional services, challenged growth, and industry worst cash flow profile suggests the downside could be even greater.

Credit: Kerrisdale Capital

The Kerrisdale Short Report

On March 6th, Kerrisdale Capital – “a research-oriented investment firm” – published a 27-page short report that rightly pointed out how shares of C3 benefited tremendously from the hype around generative AI. It also probed other concerns, some previously raised in a February 22 short report by Spruce Point Capital Management that largely surrounded C3’s largest customer, Baker Hughes, which also happens to be a related party. Yesterday’s 26% drop in share price for C3 resulted from a 7-page letter sent to C3’s accounting firm, Delloite, with a copy sent to the SEC. Said letter raised the following points of contention:

Growth in unbilled receivables

Confusing financials related to a related party and C3’s largest customer, Baker Hughes

Inflated gross profit margins that results from COGS being incorrectly classified as R&D

Classification of revenue as subscription revenue when it’s actually services

Significant turnover in CFOs who are increasingly less qualified

This aggressive escalation is understandably unnerving investors who continue to dump shares in aftermarket. It shouldn’t be a surprise to see shares sink back down to levels seen before AI hype, and this letter is only accelerating that reversion to the mean. The timing of the letter coincides with C3’s fiscal year ending on April 30, and Kerrisdale has asked Deloitte to review their concerns in anticipation of its upcoming work conducting the company’s year-end audit. Let’s look at the points of contention raised in the letter, starting with a main character in the story – Baker Hughes (BKR).

Baker Hughes and C3

With a market cap of $30 billion and 2022 revenues of $21 billion, Baker Hughes is one of the world’s largest oil field services companies. They’re also the second largest shareholder in C3 holding 8.65 million shares or about 8% of the company. (That’s after they sold approximately 2.2 million C3 AI Shares at around $66 a share in 2021.) The two companies established a joint venture in 2019 and the resulting relationship has been difficult to describe at best.

The letter’s first concern surrounds the growth in unbilled receivables which is primarily due to one customer – Baker Hughes – who is not being billed for revenues that have already been recognized. Sympaq tells us that “when unbilled receivables occur, it is because they cannot be billed yet under the terms of a contract,” and, “unfortunately, auditors view unbilled A/R with scrutiny.” Kerrisdale states the problem succinctly:

In the last four quarters, C3.ai has apparently recognized $80m of receivables (from a related party shareholder, no less) in an amount that is equivalent to almost 30% of total company-wide revenue during that same period, for which it has not even invoiced.

Credit: Kerrisdale Capital

Baker Hughes is not only C3’s second biggest shareholder, but also responsible for a third of total revenues. Consequently, they’ll be receiving favored treatment during contract negotiations. This problem is easily rectified if Baker Hughes starts being billed for the work being performed and pays those bills. If C3 is indeed “using highly aggressive accounting in order to meet sell-side analyst estimates,” then working with their second biggest shareholder to solve this problem should be an easy fix. But the much bigger problem to solve here would be properly articulating the relationship between the two parties. Some of the verbiage currently used to describe the relationship is impossible to decipher, and consequently viewed with suspicion. Kerrisdale points to revenues from Baker Hughes that aren’t being recorded with an accompanying cost of goods sold (COGS) which artificially inflates C3’s gross margin.

The Gross Margin Problem

Software companies with recurring software sales and high gross margins can rightly deserve high multiples, as operating expenses can be easily ratcheted down. But in the case of C3.ai, we believe theycan’t be.

Credit: Kerrisdale Capital

Gross margin is one indicator we look at when it comes to the survivability of any business. When times get tough, profitability can be quickly achieved by cutting costs. The higher the gross margin, the easier it is to achieve profitability. Accounting systems ensure that COGS is correctly allocated such that gross margin can be correctly calculated. If a company chooses to move COGS into another bucket, say R&D, then they would have a deceptively high gross margin. Last quarter, C3 spent as nearly as much on R&D as revenues received – about $55 million – which also happens to be the amount of shares based compensation (SBC) they paid out (typically in the tech industry, SBC would average around 23% of total revenues, a number considered high by historical standards)

We believe that C3.ai is hiding costs within research and development expenses that should be classified as costs of revenue.

Credit: Kerrisdale Capital

The implication is that C3 isn’t offering a scalable software-as-a–service (SaaS) solution, but rather a solution that requires a great deal of manual intervention. Even though they classify revenues into two buckets – subscription and professional services – C3 describes their subscription label as “stand-ready COE support services” and “maintenance and support services.” All the confusion around the Baker Hughes relationship doesn’t help here.

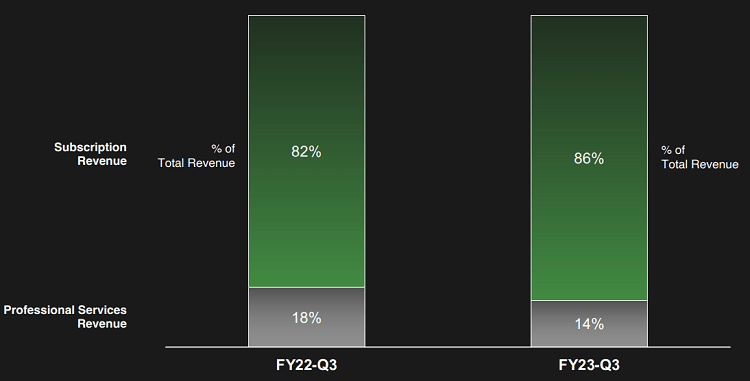

The implication is that services aren’t scalable, and C3 shouldn’t command a SaaS premium if services account for a greater percentage of revenues than what they’re stating below.

Professional services are “typically a fixed-fee engagement with defined deliverables and a duration of less than 12 months.” Onboarding new customers would be a classic example of professional services, so the number should be declining over time as seen above – unless, of course, it’s being incorrectly stated.

All the points of contention raised so far surround alleged accounting irregularities, and the icing on Kerrisdale’s cake is the high level of CFO turnover seen at C3 – 4 different chief financial officers over the last four years – each with a decreasing amount of professional experience. The implication is that no competent CFO would risk ruining their reputation by getting involved with a company that’s fudging their numbers.

Our Take on C3

Short reports need to be taken with a grain of salt, but two consecutive short reports are concerning as they largely surround points of contention that we find to be red flags as well – customer concentration risk and related party revenues. The temporary drop in share price isn’t a concern because it was massively inflated to begin with. What’s concerning is the letter sent to third parties about accounting irregularities. With the SEC in copy, Deloitte has now brought in their legal team and moved to CYA mode. It’s likely their thoughts will be made clear when we see how the year-end filings might change to explain what the short firm views as deficiencies. They’ll probably take all the time they need to conduct due diligence before signing off on C3’s yearly financial statements. C3 can say whatever they want but it’s Deloitte who we’re watching.

Deloitte doesn’t need to rubber stamp fraudulent accounting. Either require the company to come clean in its upcoming audit or resign and let C3.ai management sully the reputation of a lesser audit firm.

Credit: Kerrisdale Capital letter to Deloitte

As for C3, they made a bog-standard statement to CNBC about how “the Kerrisdale Letter appears to be a highly creative and transparent attempt by a self-acclaimed short seller to short the stock, publish an inflammatory letter to move the stock price downward, then cover the short and pocket the profits.” To be fair, Kerrisdale is correct to call out the rise in C3 shares resulting from the generative AI hype. The good news is that if Deloitte finds no fault in how C3 has been doing their financial reporting, then it’s a nonevent, and Kerrisdale’s original short accusations will lose credibility. We’re not necessarily convinced that’s the case, but we’re not here to speculate. Should Deloitte find problems with C3’s accounting, shares are going to fall a whole lot further than they did yesterday.

Conclusion

A second short report followed by an accusatory letter to one of the world’s biggest accounting firms with the SEC in copy is bad enough. Couple that with a share price that’s been pumped up over 100% because of generative AI hype and let the volatility commence. Shares of C3 should be expected to arrive at the price range they were trading at prior to all the hype. The ground truth will be in what Deloitte ends up signing off on for C3’s Fiscal 2023 results. We don’t expect much color until that happens. As for our own holding, we’re not taking any action until we hear from Deloitte, a firm that’s likely to conduct lots of due diligence before arriving at a conclusion. This situation underscores the importance of avoiding related party revenues and high customer concentration risk when investing in disruptive tech companies.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!

[ad_2]

, Lowe’s (LOW): What do these home improvement retailers anticipate for the future?")