zhengzaishuru

Energy stocks have not participated in the strong Q4 rally. Stocks bottomed out on October 27, and it was the most risk-on and rate-sensitive areas that fared the best, along with (as usual) the Mag 7 stocks. The Energy Select Sector SPDR ETF (XLE) remains down 5% since the end of September. The reason? Blame it on oil. The prompt month of WTI plunged from near $95 to below $70, but has since rebounded into the mid-$70s. It is a hopeful turn for oil and gas stocks as we head into 2024. The good news is that the Energy sector remains very cheaply priced as E&P stocks produce solid free cash flow.

I reiterate my buy rating on Devon Energy (NYSE:DVN). I continue to see shares as undervalued despite a reduced production outlook reported in its Q3 report.

Q4 Sector Performances: Energy the Lone Laggard

Koyfin Charts

According to Bank of America Global Research, DVN is an independent energy company that explores for, develops, and produces oil, natural gas, and natural gas liquids in the United States. It’s a diversified large-cap US E&P company, and fourth-quarter 2022 daily production was approximately 315,000 barrels of oil, about 150,000 barrels of natural gas liquids, and more than 1 billion cubic feet of natural gas. It operates in Delaware, Anadarko, Williston, Eagle Ford, and Powder River Basin.

The Oklahoma-based $29.4 billion market cap oil and gas exploration and production industry company within the Energy sector trades at a low 7.9 forward 12-month non-GAAP price-to-earnings ratio and pays a fixed and variable dividend, currently at a 1.8% forward yield. Ahead of earnings due out in February, the stock has a moderate 29% implied volatility percentage and a short interest of just 1.6%.

Last month, Devon reported a solid EPS beat. Q3 non-GAAP EPS of $1.65 topped estimates by $0.10, though revenue plunged 29% from year-ago levels to $3.8 billion, a small beat. The firm, as widely expected, lowered its oil production guidance, and the EPS beat was largely due to a lower effective tax rate. Its NGL and natural gas segments performed well, but reduced oil output and higher lease operating expenses offset profitability gains.

Still, overall EBITDA about matched Street expectations, while free cash flow came in a tad above estimates. It was disappointing for shareholders that the management team elected not to buy back any shares in its Q3, though it did declare a $365 million variable dividend while indicating that it might pivot to share repurchases in the quarters ahead. That could be an opportunity now that the stock is at somewhat depressed levels.

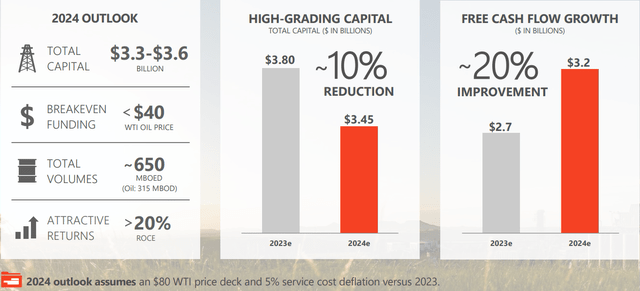

Nevertheless, analysts at Goldman Sachs see DVN shares as a value and see operational strength next year amid capital spending and oil production execution opportunities. On the Q3 earnings call, Devon’s executives said they plan FY 24 capex of $3.3 billion to $3.6 billion, slightly lower from their previous outlook. The team at Morgan Stanley seems to agree with Goldman, listing DVN as a key stock pick in the industry for 2024.

Devon’s 2024 Outlook

Devon Energy IR

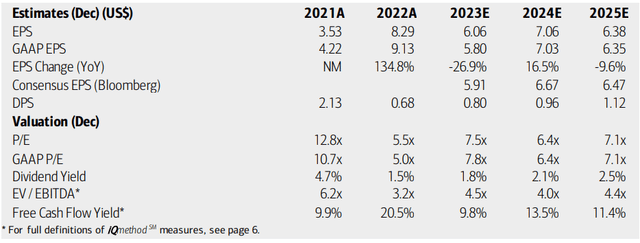

On valuation, Devon looks to put 2023’s significant operating EPS decline in its rearview mirror. Next year’s per-share profit growth is seen in the mid-double digits per BofA, though the latest consensus outlook, per Seeking Alpha, is closer to just +7%. EPS growth is then expected to home in on the $6 to $6.50 range by 2025 while top-line growth trends look rather weak, though much depends on domestic oil and gas prices.

Dividends, meanwhile, will always be volatile given Devon’s variable payout policy. The distribution rate is expected to return to $1 over the coming quarters. With an EV/EBITDA multiple under 5, there’s a significant discount to the S&P 500’s average. Finally, the stock’s current free cash flow yield is high at 9.8%.

Devon: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

BofA Global Research

Following weaker guidance in its Q3 report, if we assume normalized annual EPS of $6.40 and apply a sector median P/E near 10, then shares should be near $64 today. Also keep in mind that the stock’s 5-year average non-GAAP forward earnings multiple is closer to 12, so if there’s an uptick in oil and natural gas prices next year, I would not be surprised to see a positive re-rating across the Energy space.

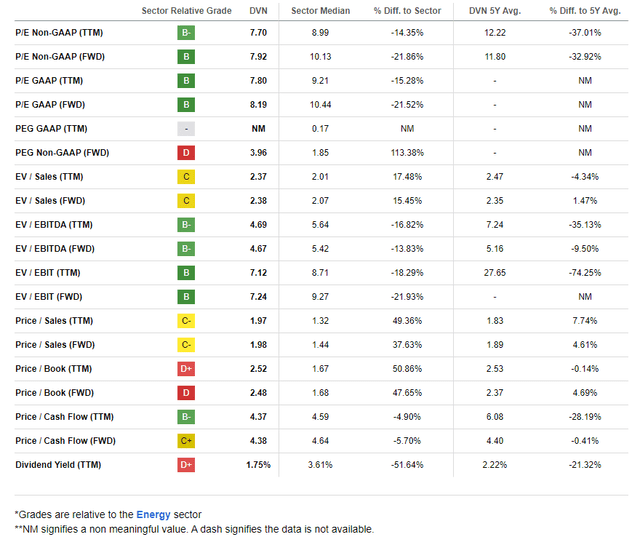

DVN: Mixed Valuation Metrics, Lower Yield

Seeking Alpha

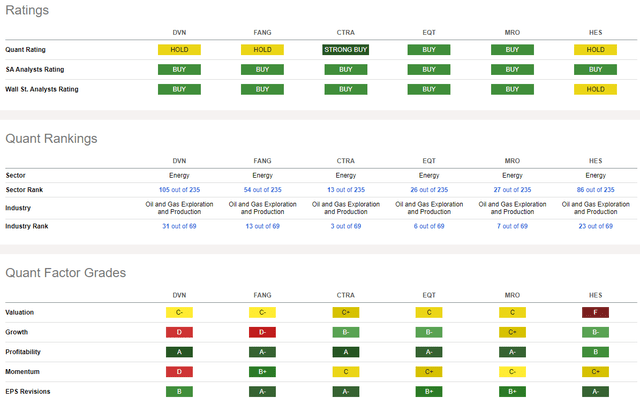

Compared to its peers, Devon features a mixed valuation rating, while its growth trajectory remains a question mark. Still, strong profitability trends and solid free cash flow are positive characteristics. Encouraging to me is the solid string of upward EPS revisions in the last several months – the last three months have brought about 17 EPS upgrades with just 7 earnings downgrades. Finally, share-price momentum has been sour throughout 2023, though I will note key support on the chart that investors, even the most fundamentally inclined, should pay attention to.

Competitor Analysis

Seeking Alpha

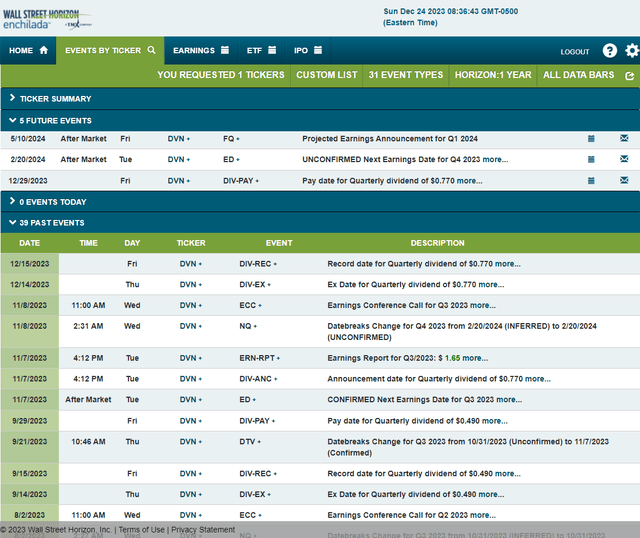

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4, 2023 earnings date of Tuesday, February 20 AMC. A $0.77 quarterly dividend will be paid on Friday, December 29.

Corporate Event Risk Calendar

Wall Street Horizon

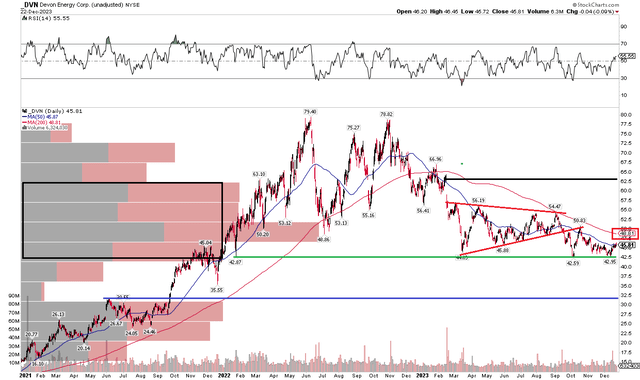

The Technical Take

DVN continues to frustrate the bulls. Notice in the chart below that shares have drifted down to key support in the $42 to $44 range. This zone has been tested on a handful of occasions since the first quarter of 2023. Rally attempts have been capped, with the long-term 200-day moving average marking a natural selling point in both August and September. With that trend indicator line sloping lower, the bears appear in control.

I am also concerned about a bearish technical pattern I pointed out earlier this year – a bearish symmetrical triangle indeed portended a move lower in the stock price. A breakdown under $42 could result in a price objective to the low $30s, based on the trading range since last February. Moreover, a high amount of volume by price from $42 up to the low $60s will make it tough on the bulls to bring DVN back into a sustained uptrend, though an old gap lingers around $62 that could eventually be filled.

Overall, the trend is not encouraging for the bulls, and I am concerned that a move under $42 could lead to a drop toward $31.

DVN: Key $42 Support, Risks To $31, 200dma Resistance

Stockcharts.com

The Bottom Line

I reiterate my buy rating on Devon. I continue to see the shares as a solid value heading into the new year but remain worried about the technical situation.