LPETTET

If you do what everyone else does, you’re going to get the same results that everyone else gets. – Charlie T. Munger

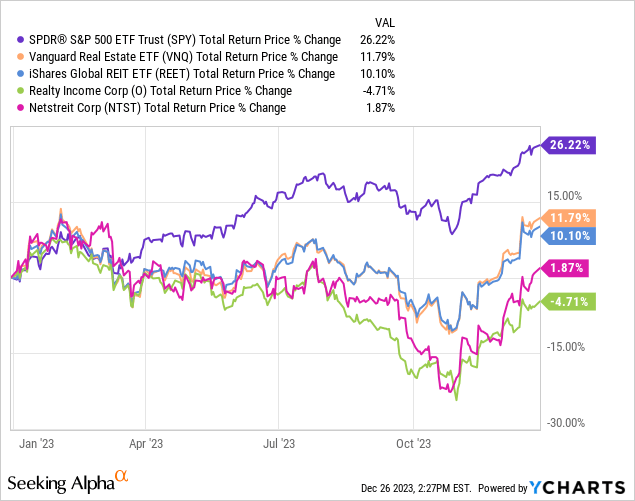

While some of the most reliable valuation indicators show the S&P 500 index in overvaluation territory, it is well known that much of the excitement is concentrated in just a few stocks. For example, Tesla (TSLA) is trading with a forward price/earnings ratio of around 80x, despite significant headwinds on the horizon. We do believe EVs will continue gaining market share over ICE vehicles, but competitive pressures will make earnings growth increasingly difficult, as we have seen with the price cuts made by the company. NVIDIA (NVDA) has delivered impressive growth, but much is probably already factored in the 40x forward price/earnings ratio, as is probably the case with Amazon’s (AMZN) 57x multiple. We will not analyze each of the “magnificent seven” companies, but as a group, they look expensive.

Still, we believe that one can almost always find a corner of the market that is either reasonably valued or undervalued. In this case, real estate in general seems to have been overly punished by the increase in global interest rates, and some solid companies like Realty Income (NYSE:O) and NETSTREIT (NYSE:NTST) have not really participated in this year’s gains.

We have covered both in the past, we started coverage of Realty Income with a ‘Sell’ rating at the end of 2021, and since then shares have delivered a total return of negative 8%, vastly underperforming. Our main point was that despite the VEREIT acquisition expected to be immediately accretive, shares were extremely overvalued. We then compared Realty Income to STORE Capital, reaching the conclusion that STORE Capital was the better value. While we were right in preferring STORE Capital, as it went to be acquired at a premium, we updated Realty Income’s rating to ‘Hold’ due to the low interest rate environment but would have been wiser to leave it as a ‘Sell’. We have covered NETSTREIT more extensively, starting with a ‘Hold’ rating, then upgrading it to a ‘Buy’, and then to ‘Strong Buy’ after Q2 results. Since then it has reported Q3 results, and Realty Income has announced the acquisition of Spirit Realty Capital (SRC) in an all-stock transaction. In this article, we are updating our analysis of both companies, considering the current economic environment and outlook and recent developments at both companies, and also explaining why we prefer NETSTREIT over Realty Income.

Investing Frameworks

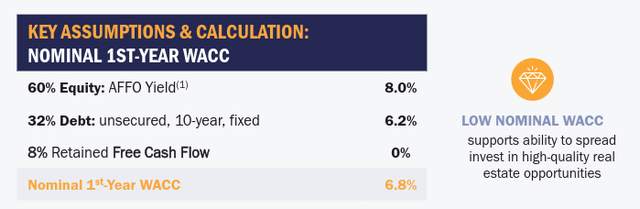

One thing we do not like about Realty Income’s investing framework is the over-dependence on a low WACC. The company itself has said that a higher stock price supports faster growth, as they require a spread on short-term WACC to generate accretion. We don’t like a growth model that depends on the share price. If anything, we prefer companies that look at a low share price as an opportunity to buy back shares.

Realty Income Investor Presentation

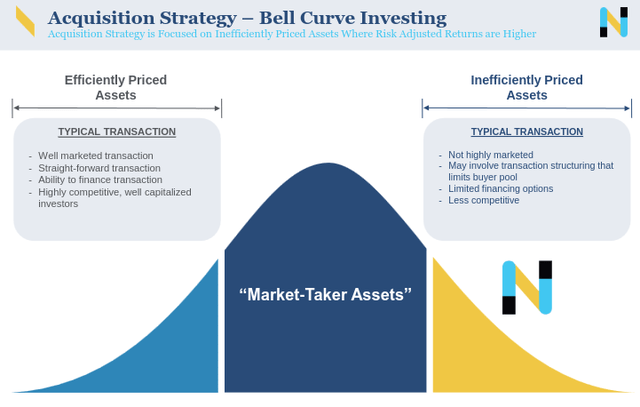

While NETSTREIT has been issuing shares when they have traded at reasonable levels to finance growth, we like that they see their competitive advantage mostly derived from their acquisition strategy.

They seek to purchase assets at an attractive cost with durable valuations supported by market rents in good locations, and alternative use potential. They also focus on more niche transactions that might be less efficiently priced, they call this bell curve investing.

NETSTREIT Investor Presentation

While Realty Income has a very strong underwriting process with a lot of historical data to guide underwriting decisions, we are particularly impressed that NETSTREIT seems to have a very solid process in place as well.

In particular, we like its three-part underwriting process, where they evaluate the tenant as most REITs do, but then follow with a real estate valuation and location analysis for the property, which includes an alternative use analysis. Finally, they check unit-level profitability, seeking a minimum 2x rent coverage and they want the property to rank in the top half of its tenant’s store portfolio.

Occupancy and Resiliency

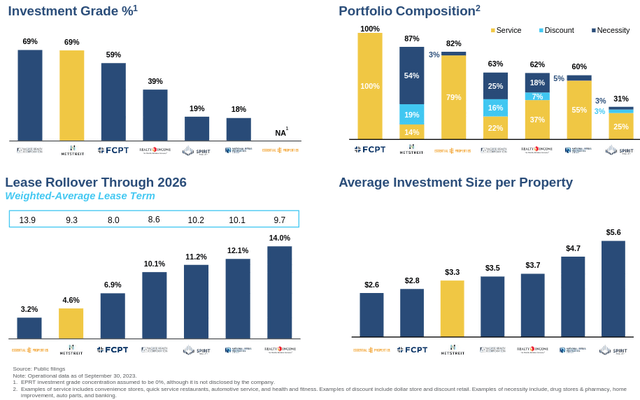

Both REITs have enviable occupancy statistics, with Realty Income ending the quarter with 98.8% occupancy, and NETSTREIT at 100%. Realty Income has a small exposure to movie theaters, which we consider a weaker type of tenant, and which affected the company when Cineworld declared bankruptcy. While the company announced in the third quarter that it had been able to recapture 85% of pre-bankruptcy rent across 41 locations, the company also has a ~1.2% rent exposure to AMC Entertainment (AMC), which is having significant issues as well. Realty Income also has significant international rent exposure, with roughly 12% of rent in the UK, whose economy is doing much worse at the moment compared to the US.

With respect to portfolio composition, we like that NETSTREIT has most of its rent coming from necessity retailers, a much larger share than Realty Income. Still, both companies have focused on resilient tenants with high stability over economic cycles.

NETSTREIT Investor Presentation

Growth

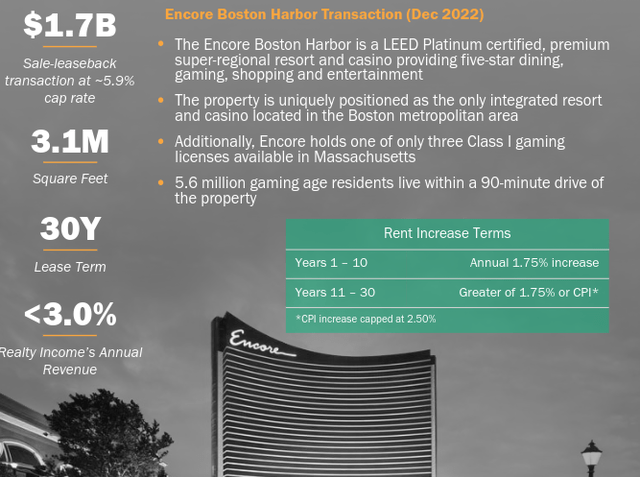

Realty Income said that thanks to the Spirit acquisition they believe they can deliver 2024 earnings growth in line with their historical average. Still, given the size and risk that comes with the transaction, we would have expected a more meaningful boost. The transaction is only expected to be over 2.5% accretive to Realty Income’s AFFO per share. Similarly, the company has engaged in some massive transactions like the $1.7 billion Encore Boston Harbor resort and casino lease-back transaction at a ~5.9% cap rate. This shows the company is increasingly deviating from its core retail competency, and receiving an unimpressive cap rate and low rent increases in return.

Realty Income Investor Presentation

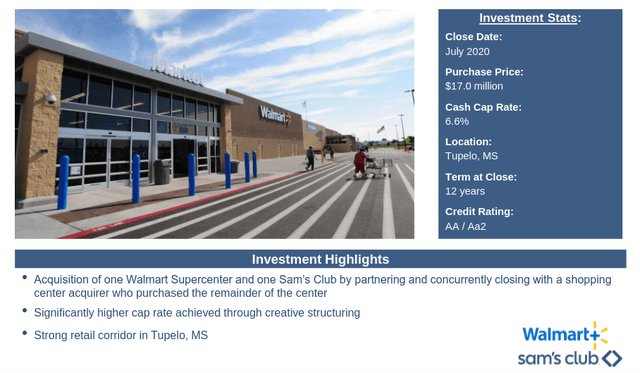

Meanwhile, NETSTREIT is showcasing retail examples like the Walmart and Sam’s Club acquisition at a 6.6% cash cap rate. More recently, it shared that its acquisitions in the most recent quarter had an average cash cap rate of 7%. The company has proven that it can invest at above-market yields without sacrificing its focus on high-quality tenants.

NETSTREIT Investor Presentation

One concern we do have about NETSTREIT is that it does not disclose much information about its average rental increases, or percentage of leases that have CPI escalation clauses. This was particularly worrying when inflation was higher but remains one of our main concerns. From what has been shared in recent earnings calls, it does seem the company is paying more attention to this issue, for example, in the second quarter of 2023 earnings call CEO Mark Manheimer said:

As we touched on earlier, we are seeing both retailers and developers consider our capital as an alternative financing option given the unattractive nature of the debt markets and/or the limited availability of financing from both small community and regional banks. While all of these market dynamics are resulting in more attractive cap rates, we’re also seeing an increased willingness by retailers, especially those committed to growing their store count, to sign leases with longer lease terms and embedded rent escalations.

In the third quarter earnings call, Mark Manheimer talked about the possibility to recycle assets to improve lease terms.

I would expect the dispositions to ramp up a little bit here in the fourth quarter, and potentially beyond the fourth quarter. We do see a pretty attractive opportunity to not only accretively recycle capital, but also extend out lease terms by replacing those assets with longer lease term assets with better rental increases and potentially better properties, and we believe we can do that accretively.

Financials

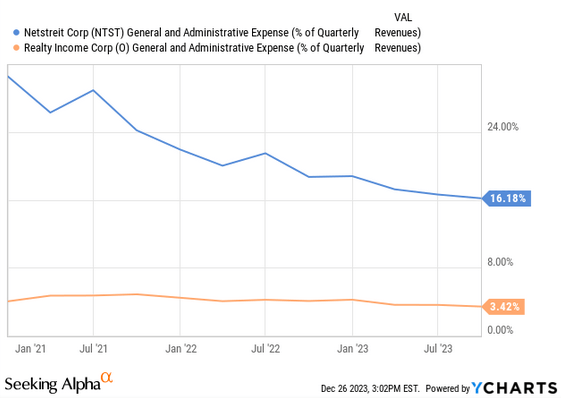

One big advantage that Realty Income has is that due to its massive size, it has gained significant operating leverage. For example, G&A as a percentage of total revenue is ~3.8%, while their median peer is at ~8.5%, and NETSTREIT is around 16%. Clearly, NETSTREIT has yet to achieve enough scale, but we see this as an opportunity, as earnings should significantly increase as it closes the gap with competitors. So far it has been trending in the right direction and at a rapid pace.

YCharts

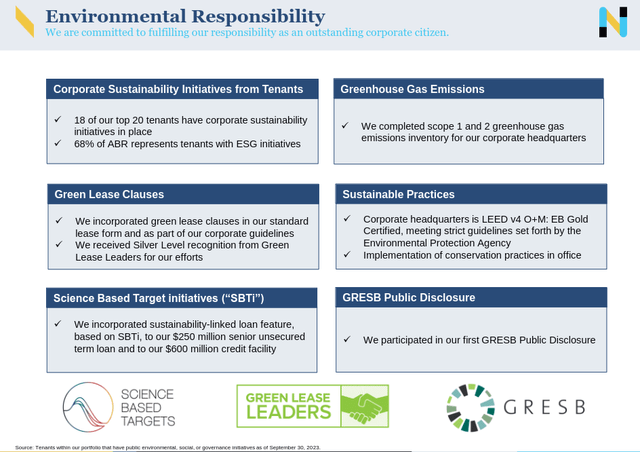

ESG

Another reason why we prefer NETSTREIT over Realty Income is that we look to avoid certain sectors like tobacco, gambling, etc. Recently Realty Income has been getting involved with the gambling industry by engaging in sales-leaseback transactions with casinos.

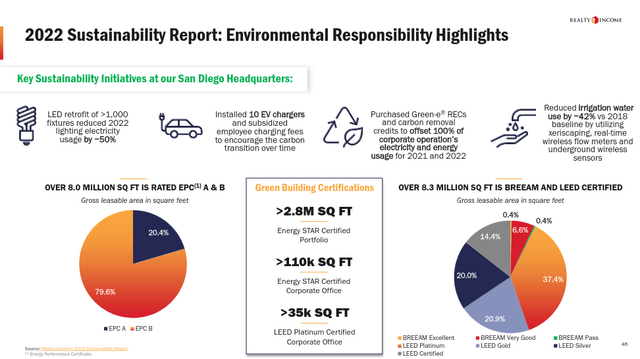

Still, we have to give the company credit for having an ESG program, and detailed sustainability initiatives as shown below.

Realty Income Investor Presentation

NETSTREIT also has an ESG program, and it even includes adding green lease provisions, and has relationships with the ESG contacts at their tenants. The company also has a sustainability-linked senior unsecured credit facility, meaning that if it delivers on certain ESG criteria it gets cheaper financing.

NETSTREIT Investor Presentation

Dividends

Realty Income is one of the dividend aristocrats (NOBL), thanks to its 29 consecutive years of rising dividends. While this is quite impressive, the CAGR is only around 4.3%, not that much higher than inflation during this time. The company is currently offering an attractive 5.4%, although the AFFO payout ratio is relatively high at ~76% and above the sector median. One advantage is that the dividend is paid monthly.

Meanwhile, NETSTREIT went about 11 quarters without a dividend increase, and only recently did it increase its quarterly dividend, raising the quarterly dividend by 2.5% to $0.205. The dividend yield is also lower, at roughly 4.6%, but the AFFO payout ratio is lower as well, at about 67%.

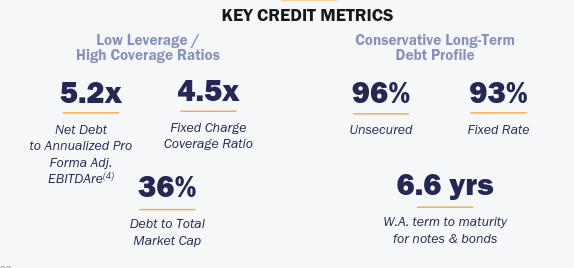

Balance Sheet

Both companies have extremely conservative balance sheets, with Realty Income having a net debt to adjusted EBITDAre leverage ratio of ~5.2x, 6.6 years weighted average debt duration, and roughly 93% of long-term debt being fixed rate.

Realty Income Investor Presentation

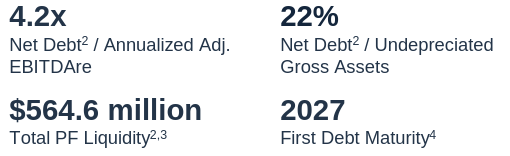

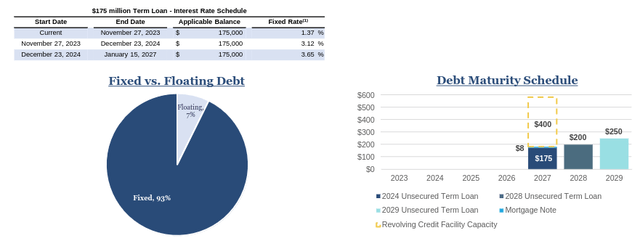

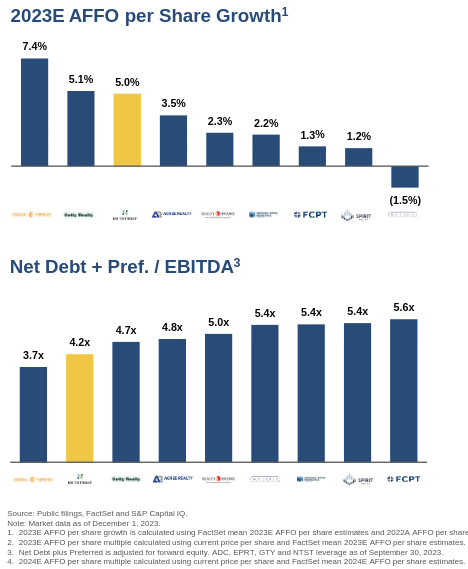

NETSTREIT is currently below its target leverage ratio, with net debt to adjusted EBITDAre leverage ratio of ~4.2x. Its target leverage ratio is to be between 4.5x and 5.5x. This means the company has room to increase leverage and boost profits.

NETSTREIT Investor Presentation

Like Realty Income, most of its debt has a fixed interest rate, it has abundant liquidity, and most of its asset base is unencumbered.

NETSTREIT Investor Presentation

Valuation

While the 2023E AFFO per share multiple is not very different between the two companies, we expect NTST to deliver better earnings growth over the coming years. Both companies faced higher financing cost headwinds this year, but NETSTREIT is expected to finish the year with roughly twice the AFFO growth compared to Realty Income.

We see several factors in favor of NETSTREIT delivering higher growth in the coming years, including G&A operating leverage as it grows its asset base, and the possibility of increasing leverage, as it is currently operating below its target range. We believe Realty Income is fairly valued (only ~4% above our DCF estimate), and see NETSTREIT as being undervalued by ~15% according to our DCF estimate. If interest rates come down next year, we see a good chance of NTST trading closer to fair value and potentially delivering total returns above 15%.

NETSTREIT Investor Presentation

Risks

We believe both Realty Income and NETSTREIT to be lower-than-average risk REITs, with resilient and diversified tenants, and strong balance sheets. Some investors will find comfort in Realty Income’s much longer historical track record, and that is fair enough. NETSTREIT has been a public company for a relatively short period of time and has yet to create a similar track record. Still, we see NETSTREIT as offering a bigger margin of safety to fair value.

Conclusion

The S&P 500 index delivered an incredible performance in 2023, while sectors like real estate that are interest-rate sensitive delivered more modest gains. Looking in more detail, some high-quality REITs are ending the year with near flat performance. These include Realty Income and NETSTREIT, which are likely to benefit if interest rates are lowered next year. While each of these two REITs has some advantages and disadvantages, overall we prefer NETSTREIT, and it is our top REIT pick for 2024. We are maintaining our ‘Hold’ rating for Realty Income and ‘Strong Buy’ for NETSTREIT.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2024 Long/Short Pick investment competition, which runs through December 31. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!