[ad_1]

J. Michael Jones

Investment thesis

Our current investment thesis is:

Winmark is an incredibly attractive niche. Management has positioned its business model to reduce risk and maximize cash returns, which has allowed for an EBITDA-M of 65%. We believe its financial performance is sustainable, with reasonable growth ahead as new franchisees sign up and retention remains high. The key for the company is the growth rate of its brands, which will dictate long-term attractiveness and revenue growth. This appears good currently, with system-wide growth broadly in line with the industry. Given the nature of Winmark, its cash return is critical. With elevated interest rates, inventors have easy access to a risk-free rate in excess of 3%, which is Winmark’s yield. For this reason, we rate the stock a hold.

Company description

Winmark Corporation (NASDAQ:WINA) is a leading retail company specializing in franchising, headquartered in Minneapolis, Minnesota. The company operates under multiple brands, including Plato’s Closet, Once Upon A Child, Play It Again Sports, Style Encore, and Music Go Round.

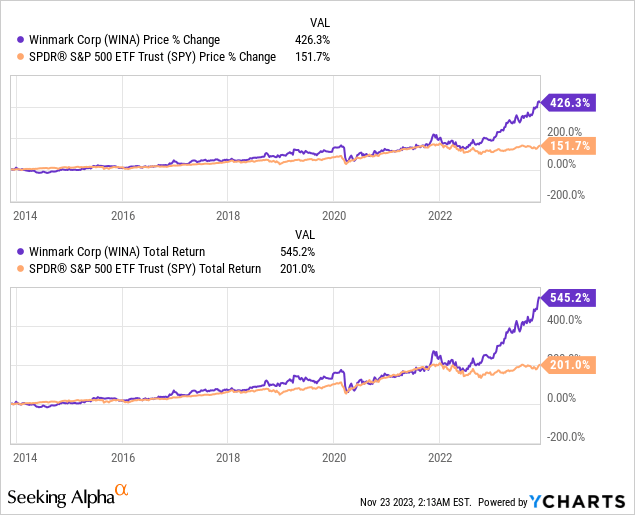

Share price

Winmark’s share price performance has been exceptional, returning over 400% in the last decade and significantly outperforming the wider market. This is attributable to its underlying fundamentals (which are very strong), alongside genuinely impressive improvements achieved.

Financial analysis

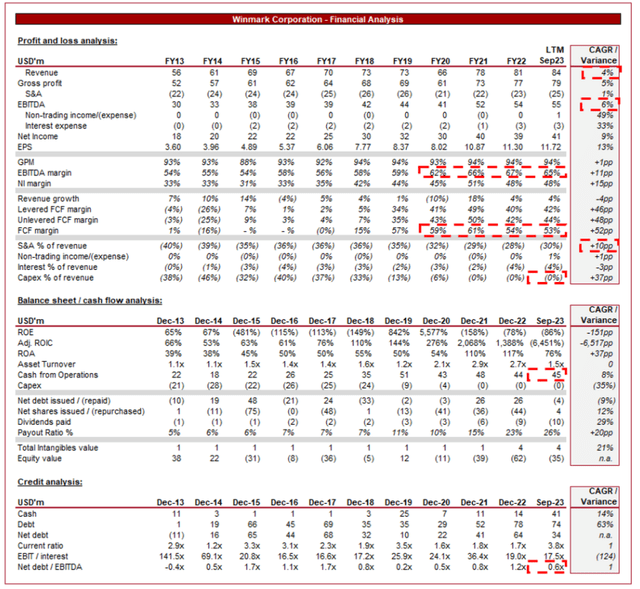

Winmark financial performance (Capital IQ)

Presented above are Winmark’s financial results.

Revenue & Commercial Factors

Winmark’s revenue has grown well during the last decade (+4%), broadly tracking in line with its franchisees. This positive development is attributable to strong brands and industry tailwinds.

Business Model

Winmark operates several franchise-based resale store brands, including Plato’s Closet (teen and young adult clothing), Once Upon A Child (children’s clothing, toys, and accessories), Play It Again Sports (sports and fitness equipment), Style Encore (women’s clothing and accessories), and Music Go Round (musical instruments and equipment).

Its business model revolves around buying and selling gently-used items, offering customers quality products at a lower price point. This niche focus has allowed it to tailor its product and marketing strategies to its specific demographic, reducing competitive pressures.

Winmark stores operate on a consignment and trade-in model, where customers can sell their gently used items to the store in exchange for cash or store credit. These items are then resold.

Winmark’s franchises are initially signed on for 10 years, with an initial fee of ~$25k and royalties of 4-5%. Inventory is managed by franchisees, which is an important distinguishing factor given the potential issues that come with working capital management over a lifecycle. The company provides comprehensive training, ongoing support, and marketing assistance to its franchisees. The business essentially limits its involvement in the franchise and in exchange does not charge an exorbitant fee. Given the de-risking profile (namely inventory and 10Y agreements), we like this approach.

The Secondhand industry has experienced an uptick in recent years, although is part of a broader growth story. The trend has grown on the idea of “thrifting”, as consumers have sought to discover bargains and discounts. Overarchingly, a growing wealth gap in the US and stagnating wages have contributed to many trading down, allowing for a broadening of its target market. The future of these tailwinds is uncertain, although we suspect health growth will continue regardless. This also acts as a buffer against the e-commerce trend, as consumers are willing to accept having to go in-store because the value is sufficient.

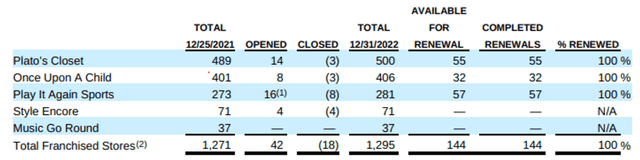

As the following illustrates, renewals have been perfect and its opening ratio is healthy, implying a good franchisee appetite for expansion (Management has stated its 10-year renewal rate is ~99%). This is a reflection of both franchisees’ outlook for growth within the industry, as well as the belief in these brands long term. This again supports the view that the future looks positive.

Stores (Capital IQ)

There is always a risk with physical retailers that consumer interests change and competition continues to increase. This is a risk that has not been eliminated, and is far from it, but a strong track record of resilience is shown. We believe Winmark’s brands are well-placed.

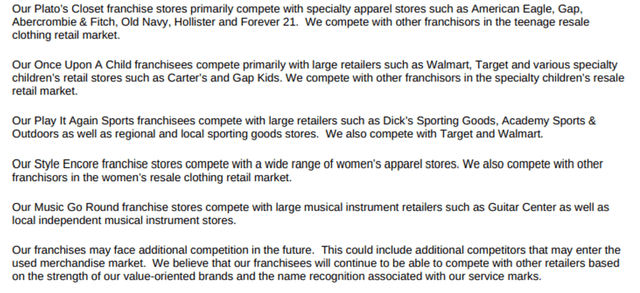

The company does a fantastic job of concisely listing the competitors of its various brands, which are presented below.

Brands (Winmark)

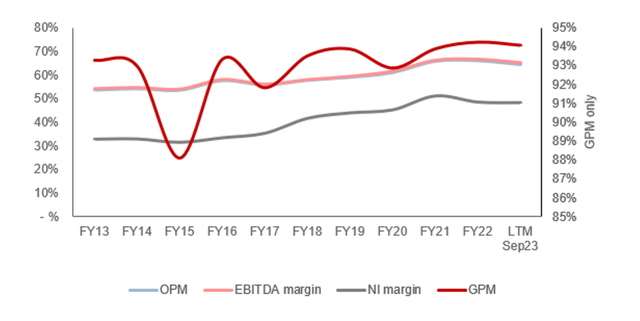

Margins

Margins (Capital IQ)

Winmark’s margins have improved well during the last decade, driven by softening operating costs relative to revenue, falling to 30% ((10)ppts). This has been driven by the benefits of scale, with operating cost leverage and scope for increasing monetization of its franchisees.

The trajectory is clearly unsustainable, although incremental improvements are likely. We suspect a target EBITDA-M of 66.5-68.5% in the medium term is reasonable.

Quarterly results

Winmark’s recent performance can be described as resilient, with top-line revenue growth of +3.7%, +2.4%, +6.8%, and +5.4% in its last four quarters. In conjunction with this, margins have stabilized from its post-pandemic high, with a small uptick in the last two quarters.

We attribute its low, but resilient growth, to the company’s business model and brand demographic. Macroeconomic conditions are currently negatively impacting the retail industry, with elevated rates and inflation contributing to reduced discretionary spending. The company’s focus on second-hand goods lends well to remain strong, as consumers are incentivized to trade down and seek bargains.

Its target demographic is the hardest hit during cyclical downturns so growth is unlikely to be incredible, however, on a relative basis, we see outperformance. Over the longer term, these downturns push people into its demographic, which is illustrated by the growing wealth gap in the US. This provides Winmark’s brand with a good runway for future growth and the ability to consolidate its position during downturns.

Key takeaways from its most recent quarter are:

In Sep23, there were 1,312 franchises in operation and over 2,800 available territories. An additional 72 franchises have been awarded but have yet to be opened as of Q3. Leasing income has softened relative to Sep22 ((26.7)%), while Royalties and Merchandise sales continue to soar (+7.6% and +33.8%). The decline in Leasing costs is a reflection of reduced equipment sales to customers and lower interest from smaller leases within the portfolio. Merchandise growth is illustrative of inherent demand within its franchises, a bullish outlook in our view.

Balance sheet & Cash Flows

Winmark’s balance sheet is incredibly clean. The company utilizes minimal debt, with a ND/EBITDA ratio of 0.6x. This allows it to maximize its cash flow return, which currently sits in the 50s. There is limited scope for variability in FCF due to the inherent demand from its franchisees to operate.

This has allowed Management to distribute to shareholders while limiting cash held, as expansion is funded primarily alongside its franchises. The business has very little need to hold assets on its balance sheet, contributing to an impressive ROA of 76%.

For this reason, investors considering Winmark should purely assess the long-term growth potential of the brands it holds. There is little to worry about operationally or even regarding stock (which Winmark has impressively negotiated out of its responsibility).

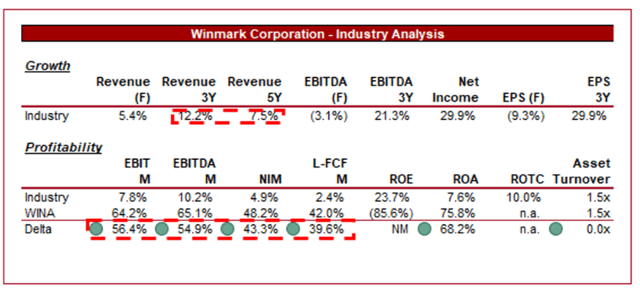

Industry analysis

Other Specialty RetaiL (Seeking Alpha)

Presented above are the growth and profitability of the specialty retailer industry, as defined by Seeking Alpha (21 companies).

The industry has experienced healthy growth in the last 5 years, owing to reasonable economic development followed by a post-pandemic bubble, funded by “pandemic checks”. Although Winmark’s brands are not “household names”, its revenue growth rate has broadly tracked the average level of its industry (~7.7%), suggesting its brands are performing well and remain attractive relative to their peers. This is critical for two reasons. Firstly, driving future royalty growth, but more importantly in our view, its ability to encourage a greater number of franchises.

The asset-light model allows for superior margins, but also a number of other benefits. The business is less exposed to cyclical swings, does not bear working capital mismanagement risks, is not directly exposed to operational risks such as employee management, and does not hold assets on its balance sheet.

With Winmark, investors can enjoy industry growth and all the upsides, with minimal downsides in a retail space that is only getting progressively more competitive. Due to this, we expect Winmark to trade at a significant premium to its peer group.

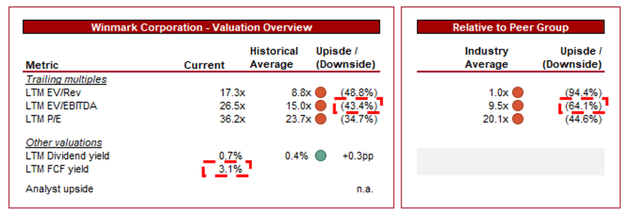

Valuation

Valuation (Capital IQ)

Winmark is currently trading at 27x LTM EBITDA, which represents a LTM FCF yield of 3.1%. This is a premium to its historical average valuation.

A premium to its historical average is warranted in our view, owing to the company’s superior margins, growth in its brands, and a greater number of franchises. Not only is Winmark a larger company, but it is fundamentally more attractive. Finally, this development has shown investors that Management can deliver on sequential improvements that are resilient.

This said we do not think the stock is attractively priced today. As an asset-light cash vehicle, its FCF yield is absolutely the most important metric. At a 3.1% yield, the business is currently underperforming the risk-free rate, while having brand risk. Even if rates were to decline below this, investors must ask themselves if they can get a better yield elsewhere with superior growth, which we believe to be the case.

Given its risk profile, which is elevated due to the fickle and volatile nature of retail, we suggest an attractive level of 4-6%. This said we concede that we are generally more conservative than the average investor.

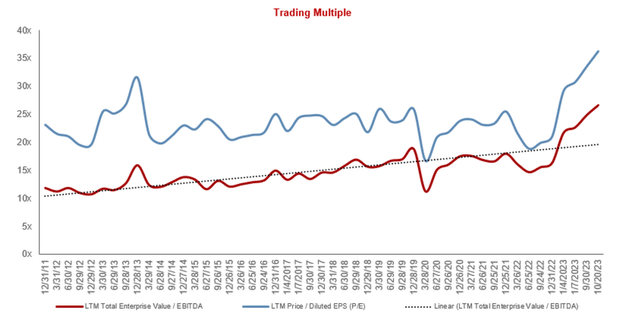

The following reflects Winmark’s valuation progression during the last decade. This is worth highlighting as, so long as margin improvement can be achieved, investors will keep pricing a premium. See our risk section below for factors that could impact this trajectory.

valuation evolution (Capital IQ)

Management

We should note that the company is not publicly covered by Wall St. analysts, lacking consensus forecasts and a PT. This is a big risk as it reduces scrutiny of Management and means there is limited ongoing analysis of the company’s progress.

For many, this is rightfully a major issue. We highlight this as a major risk for any prospective investors.

Although we do not like this as an offsetting factor, it’s worth highlighting that Management owns a considerable level of stock, aligning incentives with the wider shareholder base.

Key risks with our thesis

The risks to our current thesis are:

[Upside] Effective online expansion by its brands. [Upside] Acquisition of a growing brand. [Downside] Economic recession (near-term impact). [Downside] Failure of its brands to adapt to changing consumer behaviors. [Downside] Pressures from franchisees for better terms.

Final thoughts

Winmark is a highly attractive business in our view, operating a quality niche. The business model is fantastic, acting as a cash generator with minimal costs and no real hard assets. At a corporate level, we see minimal risks/concerns.

The key for the company is the continued attractiveness of its brands. We believe there is a good argument to suggest this, given the positive trends experienced by the second-hand industry. With continued financial struggles for millions ahead, this trend appears to have staying power.

Winmark is currently expensive, with its cash returns not sufficient in the current environment. The risk-to-reward balance is not attractive.

[ad_2]

Source link

")

")